Is it wise to invest in a Nifty Large Midcap 250 Index Fund? This question sounds so simple. But it’s not!

An investment decision can be termed wise only if it benefits you. But to know whether it has actually benefitted or not, you may have to wait for long. In other words, you can term an investment decision as wise or unwise only with the benefit of hindsight.

What if no benefit of hindsight is available? In this case, you can look at multiple factors that may affect the investment decision, including your personal investment profile (risks, goals etc.) and try to make a logical conclusion.

Moreover, before making an investment decision, you need to ask yourself a question: Do I really need this? This review of Nifty Large Midcap 250 Index funds aims to help you answer this.

But first, let’s address the Elephant In The Room i.e. the Index itself.

What’s this Index?

While choosing to invest in an active mutual fund scheme, you have the fund manager’s track record as one of the guiding lights. In a passive fund, however, the biggest deciding factor is the index itself. Therefore, when making passive investments through mutual funds, you should try to understand the underlying index first, and in as much detail as possible. This brings me to the index we are discussing in this article – ‘Nifty Large Midcap 250 Index’.

Nifty 100 + Nifty Midcap 150 Index = Nifty Large Midcap 250 Index

You can use a Nifty Large Midcap 250 Index Fund for exposure to both large and midcap stocks at one place. It is meant to reflect the performance of a portfolio of 100 Large Cap and 150 Mid Cap companies listed on NSE. The index has 100 stocks from Nifty 100 and 150 from Nifty Midcap 150 indices. The aggregate weightage of large and mid cap stocks in the index are capped at 50% each and it is reset every quarter.

If you invest Rs 5000 in this index then Rs 2500 will mostly be allocated towards the top 100 large cap companies and the remaining Rs 2500 in the next 150 mid cap companies.

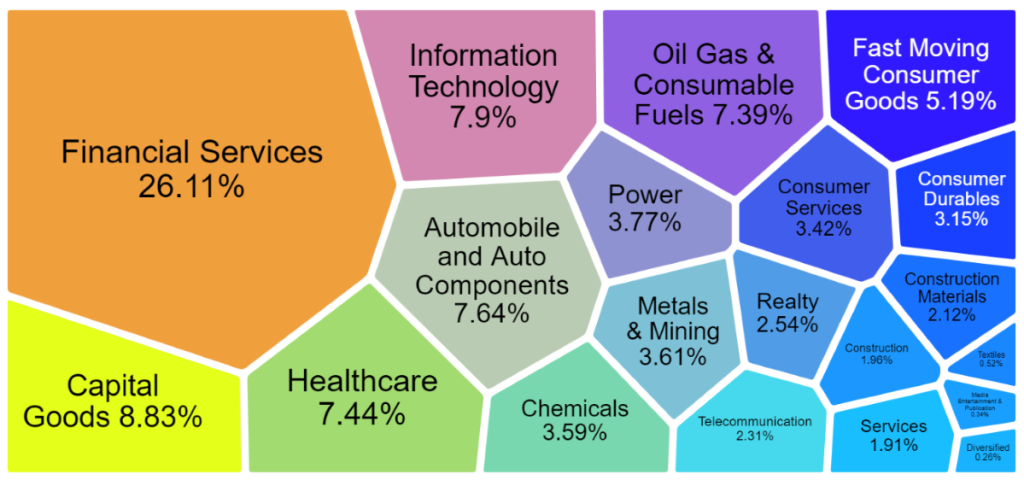

Nifty Large Midcap 250 index covers almost 84% of all the traded equity stocks at NSE. The largest sectors in this index are Financial Services, IT, Capital Goods and the top four sectors carry 52% weightage.

As per Niftyindices.com, this index is less concentrated than Nifty 100 and Nifty Midcap 150 indices, where the combined weight of top four sectors is nearly 66% and 54% respectively. It has higher exposure to sectors like healthcare, capital goods, chemicals and consumer services compared to Nifty 100. It also has more exposure to sectors like Financial Services, IT, Oil,Gas & Consumable fuels sectors compared to Nifty Midcap 150 index.

As on 29th September 2023, the total weight of top 10 stocks in the index was 24.6%. And the top 10 stocks were:

| HDFC Bank (5.62%) | Larsen & Toubro (1.79%) |

| Reliance Industries (3.89%) | TCS (1.77%) |

| ICICI Bank (3.27%) | Axis Bank (1.44) |

| Infosys (2.51%) | Kotak Mahindra Bank (1.25%) |

| ITC (1.93%) | Bharti Airtel (1.15%) |

Do You Need This Fund?

One question you should ask yourself at this point: Do I really need a fund which is exposed to both large and midcap stocks at one place?

AMCs selling funds based on this index say that the presence of both large cap and mid cap stocks provides better diversification and balance between risk and return in the long term. But this may not be true all the time, especially in the short term due to the presence of more volatile midcap stocks.

Markets perform in cycles. There are times when mid-caps or smaller companies do better while large caps underperform. Sometimes the reverse happens. In times of crash or sudden downturn, however, midcap stocks are likely to fall faster than large cap companies.

Net-net, your money in this index fund will constantly face the volatility of both large and mid cap stocks at one place. This may not be the case when you invest in a pure large cap and a pure mid cap index schemes separately.

How has this index performed?

The past performance of indices shows that returns of Nifty Large Midcap 250 index is slightly better than Nifty 50 but lower than Nifty Midcap 150 index.

| 5 year return (%) | 10 year return (%) | |

| Nifty 50 TRI | 15.34 | 13.38 |

| Nifty Large Midcap 250 TRI | 21.46 | 17.32 |

| Nifty Midcap 150 TRI | 26.72 | 20.51 |

This Mutual Fund calculator shows if you had invested Rs 10,000 in Nifty Large Midcap 250 TRI 10 years back, it could have grown to Rs 49,399. However, if you had invested Rs 5000 each in Nifty 50 and Nifty Midcap 150 separately 10 years back, your combined investment in both indices would have grown to total Rs 49,852 (Rs 17,552+Rs 32,300). Investing separately might have given slightly higher returns.

Please note this calculation is based on past performance, which may not hold true in future. Also, you can’t make a wise decision based on past returns! Then, how to do it?

Well, you need to ask yourself another question here – Does my portfolio need this fund?

If you are already invested in large and mid cap indices separately, then you may not benefit much by investing in Large Midcap 250 Index. If you are not investing in large and midcap indices separately, then you may go for the Nifty Large Midcap 250 index, provided you are convinced that it is going to do well in future and you don’t want to invest in Nifty 50 and Nifty Midcap 150 indices separately.

In case you are just starting your investment journey, this index may not be the right place to start with. More so, because the passive funds based on the Nifty Large Midcap 250 Index are very young. They do not have a long track record, which generally helps in making a wise decision.

Available Schemes

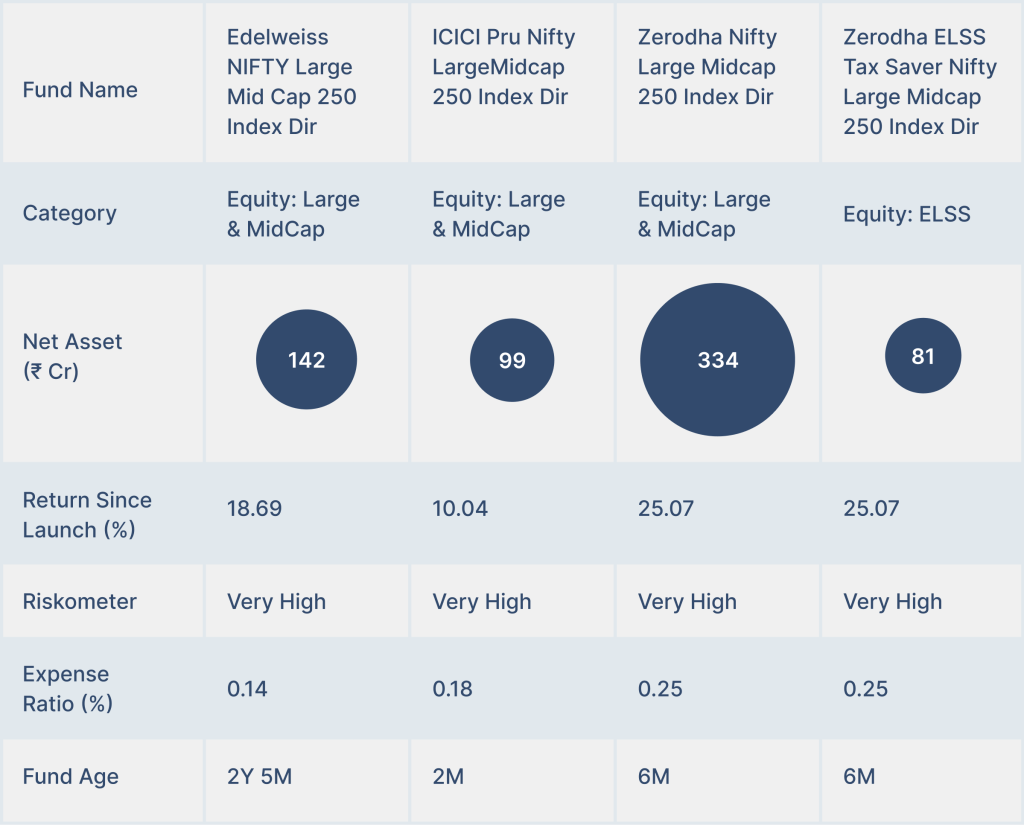

As of today, there are only four passive funds tracking the Nifty Large Midcap 250 TRI; namely –

- Edelweiss NIFTY Large Mid Cap 250 Index Fund

- ICICI Pru Nifty Large Midcap 250 Index Fund

- Zerodha Nifty Large Midcap 250 Index Fund

- Zerodha ELSS Tax Saver Nifty Large Midcap 250 Index Fund

All these passive schemes track NIFTY Large Mid Cap 250 Index TRI (Total Return Index). However, none of these four funds has a long history to provide you enough benefit of hindsight. They are all new funds launched in the last two years. In fact, the oldest scheme of the four is Edelweiss NIFTY Large Mid Cap 250 Index Fund, launched 2.5 years ago, while twin schemes of Zerodha AMC were launched 6 months back and ICICI Pru’s index fund two months back.

Schemes’ AUM

It is interesting to note that despite being in existence for 2.5 years, Edelweiss’ AUM has reached just Rs 142 crore while Zerodha’s scheme has attracted an AUM of over Rs 334 crore in just six months. And ICICI Pru has got to Rs 99 crore AUM in 2 months!

Higher AUM, however, doesn’t say much about the quality of a fund as it can be an outcome of clever marketing as well.

Expense Ratio

In terms of expense ratio, Zerodha’s schemes are costly (0.25%) while Edelweiss’ fund is least expensive (0.14%) and ICICI Pru’s plan is in the middle (0.18%).

Comparing these index schemes’ basis expense ratio alone will also not be very helpful. More so in this case where the difference in expense ratios is not very much.

Returns

Funds are often judged by their performance. But it’s meaningless to make a return-based comparison of schemes that are not even more than 2.5 years old. Moreover, you can’t even make an investment decision based on a scheme’s past returns only

Final words

Nifty Large Midcap 250 Index fund allows you to play with a combination of large and midcap stocks. There are also multiple active funds tracking this index. But if you feel actively managed funds can’t do the job efficiently, you might opt for a Nifty Large Midcap 250 Index fund. However, before making the decision, you should ensure that your portfolio really need this fund and you understand the risks.

Large and Midcap stocks in Nifty Large Midcap 250 Index have 50% weightage each. However, there is a problem. If midcap stocks are doing well, this index might look great. If not, it would appear terrible compared to Nifty 50 index.

For someone who like to keep things simple, investing separately in Nifty 50 and Nifty Midcap 150 indices may make more sense than putting all the money in one scheme. However, it is advisable to do a thorough analysis of one’s portfolio, financial goals and and risk appetite to decide whether this fund is suitable or not.

Disclaimer: The above content is for informational purposes only. Please consult a SEBI-registered investment advisor before investing.